Category: Apprentice VC

Latest book :: Amp It Up

Picked this up today at Kino

Amp it Up by Frank Slootman : https://amzn.to/3H70IV1

My ex WebLogic buddy works at https://shv.com/ so have always followed their incubation projects of which Snowflake, Pure Storage and Sigma is all from that.

Was excited to see what Frank has to say…

Review later…

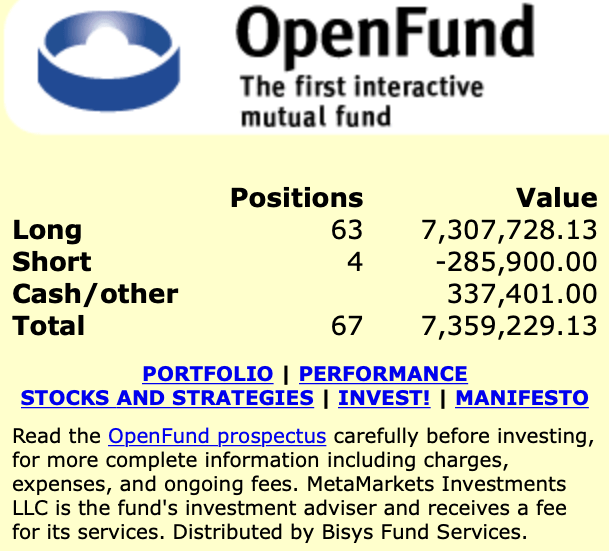

Open Everything

My history with things being “open” started in 1999 when I was the CTO for MetaMarkets.com – first Startup to run a real mutual fund out in the “open”.

https://web.archive.org/web/19991012082412/http://metamarkets.com/

We raised a huge chunk of change, 17M USD, and when it all failed I got to wheel my Aeron chair down the street to my SF loft. It was bleeding edge for the open trend and was just a bit too much.

Now you see more and more Open Startups – my favorite is:

https://www.bannerbear.com/open

Fun to follow for the tech, the business advice and watching him consistently grow the company. Impressive.

Now – Open VC. This is super impressive.

https://www.blackbird.vc/returns

I wonder how many more VC’s will do it – guessing not many. Most don’t have those kind of returns so that helps but I think most jut don’t want to share.

I love this trend though and I think as Web3 starts to take hold – more of more of this type of open will happen.

Great Post from Reid Hoffman on boards

When I started as a VC I was trying to read everything about boards – it was the one thing I was worried about. I had experience with everything else but not sitting on a board. There are not many good books on it either.

This is one of the better threads I have seen on it and a nice doc for it.

Takes time to learn to become a good board member but helps to have some direction. My other advice is ask to join board meetings of larger companies so you can see how it works.

After more than 1,000 board meetings at Microsoft, Airbnb, LinkedIn, PayPal, and more…

I've learned that effective boards don't happen by accident.

Here are 8 rituals of the world's best boards: 👇

1. Be inclusive.

Many board meetings are dominated by one or two board members.

The best boards seek out the opinions of everyone in the room, not just the loudest.

2. Fundraise proactively.

Most boards reactively raise money when the company runs out of cash.

The best boards proactively plan for fundraising opportunities like market shifts and inbound offers.

3. Advise, don't pilot.

The worst boards can break a company by dictating priorities.

The best boards take a hippocratic oath of "do no harm". They aren't pilots. They're front-seat advisors.

4. Hire for cofounder mindsets.

The best boards understand this secret to hiring great executives.

People with a cofounder mindset are willing to take risks when success isn't guaranteed.

5. Invest in relationships.

Hollywood idolizes board meetings as the place where crucial decisions are made.

The truth is the best ideas, collaboration, and feedback happen outside the boardroom in informal 1:1 meetings.

6. Tap into individual superpowers.

Everyone has a superpower — a unique combination of skills, experiences, strengths, and networks.

The best boards leverage the superpowers of individual board members, to help the company navigate threats and unlock opportunities.

7. Send personal emails.

How would you feel if you got a personal email from someone on the board of your favorite company?

The best boards send personal emails to help the company sell, hire, and raise money.

8. Think big.

The best boards are the CEO's biggest cheerleader. They inspire the company to stretch the limits of what's possible.

Airbnb famously did this by designing an 11-star experience for guests.

You don't have to wait until your company is as large as Microsoft or as ubiquitous as Airbnb to create a world-class board of directors.

Start today.

I’ve turned these 8 rituals of great boards into a set of tools you can copy and use.

Originally tweeted by Reid Hoffman (@reidhoffman) on November 18, 2021.

Josh Wolfe from Lux shares his redacted Quarterly Report

There is a ton in this. I will have to sit and read all the docs.

Full thread in the post!

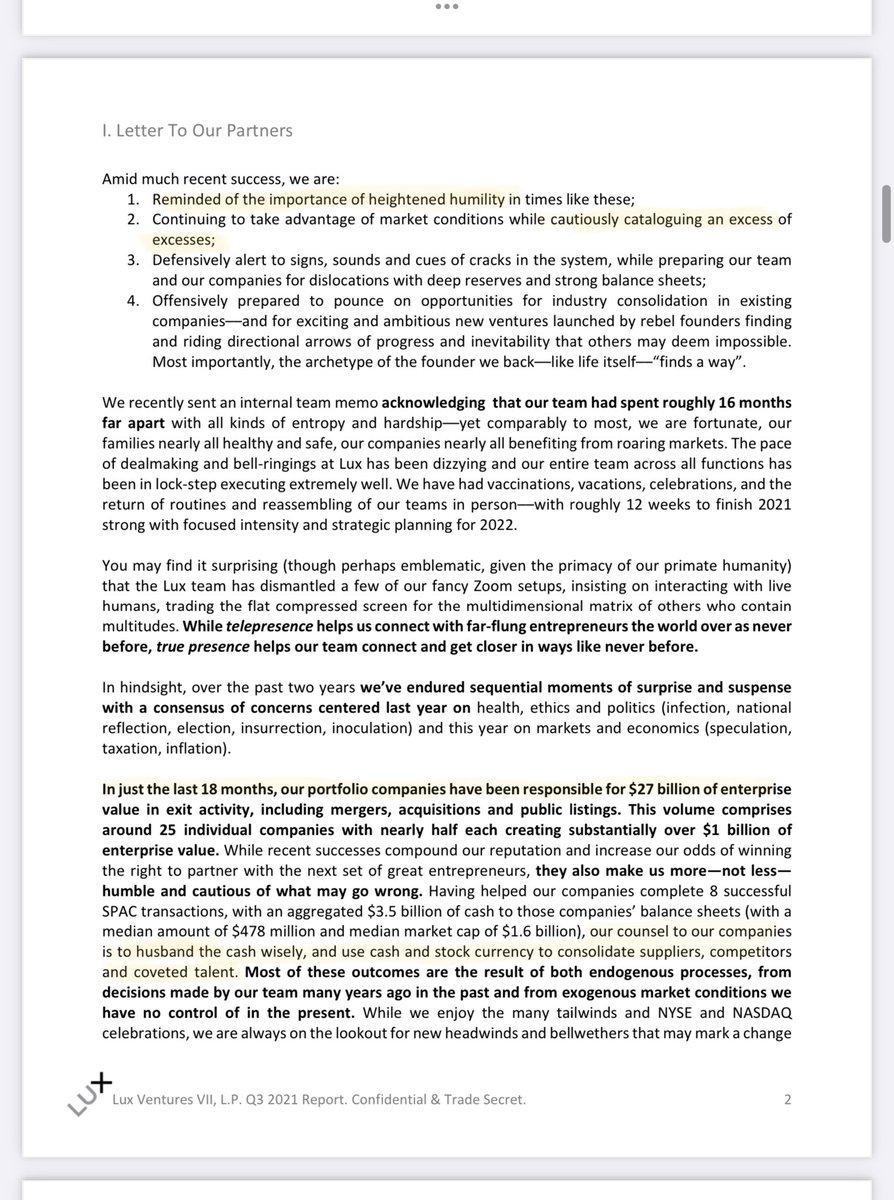

1/ Releasing a redacted Lux quarterly letter to LPs.

Some strong views of

-a catalog of an excess of excesses

-what catalysts cause the current market frenzy to end

(preview: LP indigestion)

-what we are advising our Lux family companies

-much more…

2/-The importance of HEIGHTENED HUMILITY in times like these (where source of ‘success’ can be easily mistaken)

-Telepresence helps us connect with far-flung founders but true presence (in person) helps our team connect like never before

-Where a CONSENSUS of CONCERNS is CENTERED

3/ Time travel with us a year hence—

reflecting back on the year that was.

Which of the 2 paragraphs below do you expect to read in Q3 2022?

4/-Is now time for CAUTION or throwing CAUTION to the wind?

-Valuations have risen

diligence fallen &

EXCESS is in EXCESS

-Preparing for the turn—when it comes

is wiser than predicting—when it may

5/ An excess of excesses—or what things wicked may this way come…

As Fed + central banks dole out dramatic distortion of discount rates, duration and the “true” cost of capital into markets…

A scene from ‘Deadwood’ comes to mind…

6/

-In just the last 12 weeks, startups raised more than the entire 99-00 .com boom/bust

-Character is built thru hardship + steep slopes

Yet today’s hero’s journey has given way to flattened slopes

-Thus far all news has been good news—which to realists—portends bad news.

7/ Failures comes from a failure to imagine failure

Good times let guards down

making co’s vulnerable to the silent artillery of time

LP’s whiteboard of GPs coming to market

looks like A Beautiful Mind

indigenstion of LPs + pace of new commitments

cant match pace of new raises

8/…before continuing…

ht @TheRealCarlChi1 for the image of investor swim lanes then + now

9/ The “Hemingway Hinge”…

A few funds with AUM $50-100B taking page from Carlyle,Apollo, KKR + now TPG will…

turn once cultivated intimate partnerships

into calculated intentions to go public becoming institutional corporations, fully diversified supermarkets

10/

-We have benefited from unusual demand—just as we caution against its unlikely persistence in its current form.

-we said 90% of SPACs would be CRAPs

-Some deals will prove…less kosher than a kilebasa sausage smothered in swiss cheese

-The Appointment in Samarra…

11/ Indefinitely Modified Paths—the wisdom of William James & Jurassic Park.

“Life finds a way”… and so do incredible founders

in every cutting-edge industry we find + fund…

12/

Space race is real—over 12 nations have astral aspirations

took humanity til 1961 to launch 1st 👨🚀 in space

last mo there were 14 in space @ same time

Do wise things when others are doing provably foolish things

And do what may appear to be foolish that’ll prove to be wise

Originally tweeted by Josh Wolfe (@wolfejosh) on November 14, 2021.

Appears that stuff is getting a bit frothy?

Thought this was a solid post, as usual, from Fred:

(LINK) The Great Public Market Reckoning – AVC

The Great Public Market Reckoning – AVC:

I believe that we have seen a narrative in the late stage private markets that as software is eating the world (real estate, music, exercise, transportation), every company should be valued as a software company at 10x revenues or more.

And that narrative is now falling apart.

If the product is software and thus can produce software gross margins (75% or greater), then it should be valued as a software company.

If the product is something else and cannot produce software gross margins then it needs to be valued like other similar businesses with similar margins, but maybe at some premium to recognize the leverage it can get through software.

But we have not been doing it that way in the late-stage private markets for the last five years.

I think we may start now that the public markets are showing us how.

In general private market pricing is tough but there are some guidelines. However what happens is that along the way valuations just get silly – founders and VC’s are both to blame.

To put it even more simply than Dan and Fred – the silliness is coming to an end.

Expect Southeast Asia to feel it next.

(LINK) Direct Listings: What They Are and Why VCs Favor Them Over IPOs | Fortune

Will be interesting to see if this movement takes hold and how it could come to Asia.

Venture capitalists are banding together to push the IPO alternative as a better way for startups to go public.

— Read on fortune.com/2019/09/26/what-is-a-direct-listing-vc-ipo/

(LINK) Neither, and New: Lessons from Uber and Vision Fund – Stratechery by Ben Thompson

Sounds like Ben is shifting his stance quite a bit.

Will be interesting to see that change.

Neither, and New: Lessons from Uber and Vision Fund – Stratechery by Ben Thompson:

Going forward I plan to be a lot more skeptical about other tech startups that interface with the real world and the attendant drag on margins that follows; I am not saying that the category isn’t viable, and technology truly makes these companies different than the incumbents in their space, but they are not necessarily tech companies either.

(LINK) The Hit Rate – AVC

Yup.

Returns are not as high as most people think.

The Hit Rate – AVC

— Read on avc.com/2019/09/the-hit-rate/